The market looks fairly shaky to me. I’ve already got a fair bit in shares but also have a substantial amount of cash to invest and am just sitting tight for the moment. Any clues what to do? I was thinking of putting some in gold as a safe haven,

If you don’t want a managed fund and want to pick something yourself, don’t be afraid to have a look at some defensive / lower risk funds and see where they are putting their money. All listed funds on the ASX have a top ten shares held information panel.

2 Likes

FWIW, my unhedged gold (PMGOLD) is beating all my other index funds this financial year (+8%)

The last couple months have been hilarious with it and VGE just being contrary to everything else.

1 Like

Thanks, that’s a decent return. I’ll look into that one.

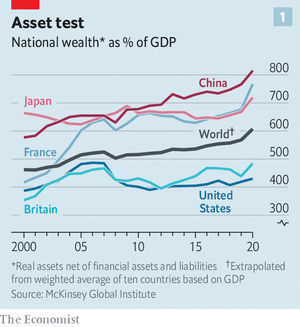

The lead article in The Economist this week says most economies are slowly ‘turning Japanese’… jeepers…may as well put your spare cash in a box buried in the backyard (hmmm…post the location of such box here on blitz… just in case ![]() ) .

) .

Why the world is saving too much money for its own good

I wont post the whole article, but here are a few bits

NB - Check France out? What on earth is going on in France?

High-rolling households have not been alone in stockpiling savings. For decades, corporations have been hoarding money as well, retaining a large share of their hefty net profits. According to Peter Chen, of the Analysis Group, an economic consultancy, and Brent Neiman, of the University of Chicago, and Loukas Karabarbounis, of the University of Minnesota, annual global corporate saving rose from less than 10% of world gdp to nearly 15% between 1980 and 2015. The corporate sector has been acting as a net lender to the global economy, rather than as a net borrower from it.

The world, in other words, may come to look ever more like Japan. There, the median age is 48, more than a quarter of the population is over 65, and the yield on a 30-year government bond is a cool 0.8%, despite a government debt load of 259% of gdp.

A generation ago, Mr Bernanke reckoned that Japan’s lacklustre growth and subterranean rates of inflation and interest were the consequence of “self-induced paralysis” by the central bank. Today, such realities seem more like the dull fate of a world with more savings than it quite knows what to do with.

1 Like

It means they can get money even

cheaper on the international money markets so there is no big reason to offer much in the way of rates on a term deposit?

1 Like

The old rich 1% are saving.

They hold all the wealth and that’s the problem.

The rest are in crippling debt squabbling over the assets that do get sold off.

Such is the curse of ever lowering interest rates.

We are in a global debt trap and the only really way out of it is to tax assets(what everyone is trying to accumulate in this thread) and redistribute it. Come at me capitalists and prove me wrong with another way.

1 Like

France c. 1789?

1 Like

This probably belongs in the housing thread but oh well. I suppose I would consider myself a “capitalist”, but I am also a first home buyer so definitely partial to your post. My view is that it is absolutely pathetic that the government has made it much easier for those who are already wealthy to accumulate even more wealth through property, than for people to get into the market in the first place. I do think you should be allowed to invest in property, but it should not be the primary purpose of housing. You’re rich and want to invest, go play on the share market or buy precious metals, it’s not as if society hasn’t provided you an avenue to invest anywhere else.

This is just one example where you can see the wealth transference happening at full speed. They have been printing money like they’re making lollies since covid, but it’s only coming to the plebs in the form of debt. The whole thing is a big joke, but it’s hardly surprising when you see the vested interests of those in power. The likelihood therefore of the establishment removing incentives to swing the pendulum back the other way is very minimal.

3 Likes

You’re speaking like “the wealthy” and “the government” are two different groups.

Ha, I should’ve phrased it differently then, as they most certainly aren’t

The problem in Australia is that the majority of voters are already land-owners, and fall into the baby boomer or older categories, and that is where elections are won and lost. So it is absolutely in the interests of Scomo and Albo, to keep those property prices soaring as it helps the majority of Australian voters. Sadly these unrealistic property price rises, come at the expense of the under 40’s who are the minority of voters, and will be paying off unsustainable mortgage debt

1 Like

Not totally sold on that analysis. Large swathes on wealthy boomers in Melbourne and Sydney who used to be liberal voters but now in open revolt.

2 Likes

Point of order…

Given WWII ended in 1945, I allow 10 years for the baby boom, meaning the boomers are >65.

I won’t accept that the majority of voters are >65.

5 Likes

Lucky you weren’t paying off mortgage debt in the late 80’s - there wasn’t much left in the kitty after paying 18% on a home loan.

3 Likes

Especially after a pandemic that is targeting this age group at a greater rate than any other age group.

1 Like

Luckily mine was limited to 13.5%

1 Like

yep would be interesting looking at the median wealth of Pollies compared to the average australian.

I mean turnball was worth millions i’m sure there are others, Clive Palmer bought his way into politics as was bored of being rich.

Clive Palmer deliberately split the Labor vote to secure his business goals.

1 Like

Just send a mass email with a link to surveymonkeys asking one question.

What is the cost of a loaf of bread, milk and a RAT?