Does the government really think there will be some financial windfall from this? Rich folks are not gonna sit by while they get taxed 30%, they’ll restructure finances.

what are there options…contribute less to super ie don’t maximise contributions, and invest in personal name where rate may be >30%

or put into trust ? / Company 30%

Im a big fan of a reasonable pension and a slab of money quarantined from everyone for your retirement.

A bit of money bankrupt proceedings, lenders, ex partners (business or personal) etc cant touch over your lifetime.

That plus a pension thats not asset assessed.

Then no matter how unlucky/how much you ■■■■ up in life with money, if you at least work and get paid you will be alright in the end and have a comfortable life when not working as reward for slaving away.

Then if you are smart, have a bit of luck in your own ventures etc and make a bit of a fortune good luck to you. Just dont expect everyone else(ie the taxpayer) to subsidise it.

Finally If you don’t at all - lose or spend it all then there is an ok pension.

You can only get so much in without it being taxed pretty significantly compared to other options. I think these big balances come from the period of time when it was a free for all.

Also money in super is limited as to what it can be invested in to some degree

Despite getting taxed for amounts over the tax free limits it still represents an attractive investment vehicle. Given the number of high paid workers I expected they’d be more. But there you go.

Were I to contribute the maximum superannuation concessional contribution every year from now (mid 40s) until 67, I might, just might, get to a balance of $3 million at 67, if I can somehow reliably get 9% average annual compound return.

That balance is based on just the employer contributions every year from age 18 until now, and with professional salary level contributions for the last 20 years (and with a subsequent break of 3 years when working OS).

To actually hit the limit, even with the heroic assumptions above, I would have to further assume that no government ups the balance limit for the next 20 years.

And for context, a balance of $3 million would generate, at a fairly conservative 5% return, a benefit of $150k per year indefinitely (i.e. without touching the capital), which under current Super rules could be received tax free. So hardly living in penury.

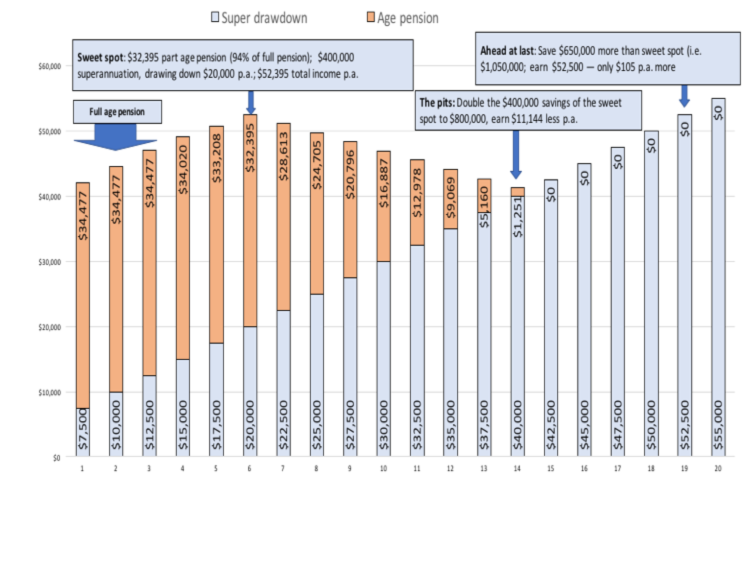

Yeah, at the moment there is some perverse “balancing” which encourages people to blow money (e.g. on a home upgrade) to get more pension.

And the above doesn’t reflect the value of discounts the couple on the pension get that the “millionaire” couple doesn’t.

Now I’d prefer to be the millionaire or even the $800K and have to spend at an unsustainable rate to not be worse off, but it’s weird. In the not-too-distant future that $400K for a couple will be the exception rather than the rule.

There are other ways to contribute beyond limits. Things like downsizing rules and small business concessions. I do remember a client who sold their taxi licence for about one million and contributed the whole thing to super within the rules at the time.

SMSF balances you need to be a bit careful how to calculate. You can have up to six members per fund. All six members can also have different balances within the SMSF.