Nancy Pelosi says hi…

2 Likes

What’s everyone biggest single position and why?

My house because I live in Australia

6 Likes

LYC because I wanted to support transition to renewables. All my other shares are mining renewables related plus Tesla.

1 Like

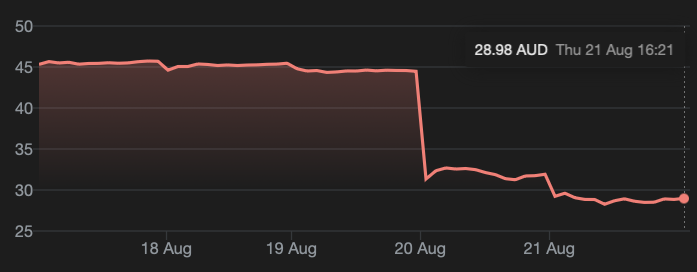

RAC. Race Oncology.

What they have will change the way multiple cancers are treated. 100% conviction.

I have been set very early, but when they release their results (which based on historical data, will be a formality) between now and probably April next year. Expect an incredible re-rate.

*not investment advice

5 Likes

Good evening, CSL investors.

1 Like

Thanks !!! I have a few and will buy more in the morning !! What a poor day though

West farmers because I can’t go into Bunnings and only buy one thing!!

2 Likes

AI Bubble..Bubble …POP!.

source: The Economist.

Among the world’s 25 biggest companies by market value—of which Palantir is one—only Nvidia, with its near-monopoly on artificial-intelligence chips, scores higher.

Chart: The Economist

Any investor would want a piece of that. The trouble is that Palantir’s market value has already soared to $430bn (see chart 1), more than 600 times its past year’s earnings and nearly triple the equivalent multiple for Cisco (or, indeed, Nvidia) at its peak. Software firms often prefer to express their valuation in terms of underlying sales, which puts Palantir’s multiple at around 120. For comparison, in 2005, the year before the Oxford English Dictionary added the verb “Google”, Google’s price-to-sales ratio peaked at 22.

The firm helps everyone from spooks to fast-food chains analyse their data better and thereby improve their operations. Its blistering recent growth comes, in large part, from enthusiasm over adopting AI for such purposes. Palantir’s competitive advantage derives not just from its software and clever engineers, but from a high-level security clearance allowing it to process classified information from America’s defence and intelligence agencies. This gives it a “moat” with which to fend off competitors.

1 Like

Let’s all dance while our stonks crater…

1 Like

Fortune has 10 zeros, not sure what that is, gazillions?

So 1% has 8 zeros, not 7

James Hardie Industries says “hold my beer”.

1 Like

Palantir’s competitive advantage derives from its utter lack of ethics combined with its closeness to an utterly unethical US president who is known for shuffling other people’s money to those individuals and organisations willing to act unethically on his behalf.

2 Likes

JHI can fark off till they pay all those mesothelioma victims what they owe them.

1 Like

One for the accountant nerds.

I am a regular PAYG person.

I have been asked to do a one off job that requires me to be paid using an ABN, and I’ll earn $4K.

It’s just one off, so I haven’t set this up as a business.

What do I need to know regarding tax? Do I now need to register as a business and do another tax return?

You’ll need to get an ABN, you are effectively in business if you invoice using it. No need to do anything else to set up as a business.

It’s just a separate section on your usual individual tax return that you will need to complete and declare it. That goes for the income and any expenses.

3 Likes

KJ is correct on the ABN, it’s pretty simple to be a sole trader with just an ABN.

the bigger issue is how are you legally protected, I presume you don’t have professional indemnity insurance and what contract covers this arrangement. If they sue you and you don’t have insurance and you aren’t a company it’s your assets on the line. You want to be very careful, $4k might be some nice cheap money but if it goes pear shaped you could lose your house. Getting proper legal advice might be worth it(I’m not a lawyer).

3 Likes

…and Dear Leader buys 10% of this quagmire.

The Economist: 21 August 2025.

To survive, Intel must break itself apart

And it should do so before it is too late

The company has missed nearly every big shift in its industry over the past two decades. It failed to profit from the rise of smartphones, was slow to adopt advanced lithography tools and has largely sat out the boom in artificial intelligence (AI). Between 2021 and 2024 revenue dropped by a third, from nearly $80bn to just over $50bn; last year it made a net loss of almost $20bn (see chart 1). Over the past five years its market value has fallen by roughly half, to around $100bn. TSMC, which has stolen Intel’s crown as the world’s leading chip manufacturer, is worth ten times as much.

Evercore, an investment bank, reckons Intel’s design arm might be worth more than $100bn on its own. But it faces a crowded field and its products are no longer distinctive.

Mr Tan could sell the division to another fabless chipmaker such as Broadcom while it still holds value and focus solely on the foundry, which is troubled but holds more long-term promise. Its newest “18A” process incorporates transistors that are ahead of TSMC’s, as well as a novel way of feeding power through the back of the chip to save space and energy. SemiAnalysis, a consultancy, reckons Intel will need to invest a bit over $50bn between 2025 and 2027 to make it competitive in leading-edge manufacturing. A sale of the design division would more than cover that.

1 Like

Didn’t buy - was bribed/gifted 10%.